From Insights to Action: The New Operational Mandate for AI

Dec 23, 2025 by: Bart Modrzynski

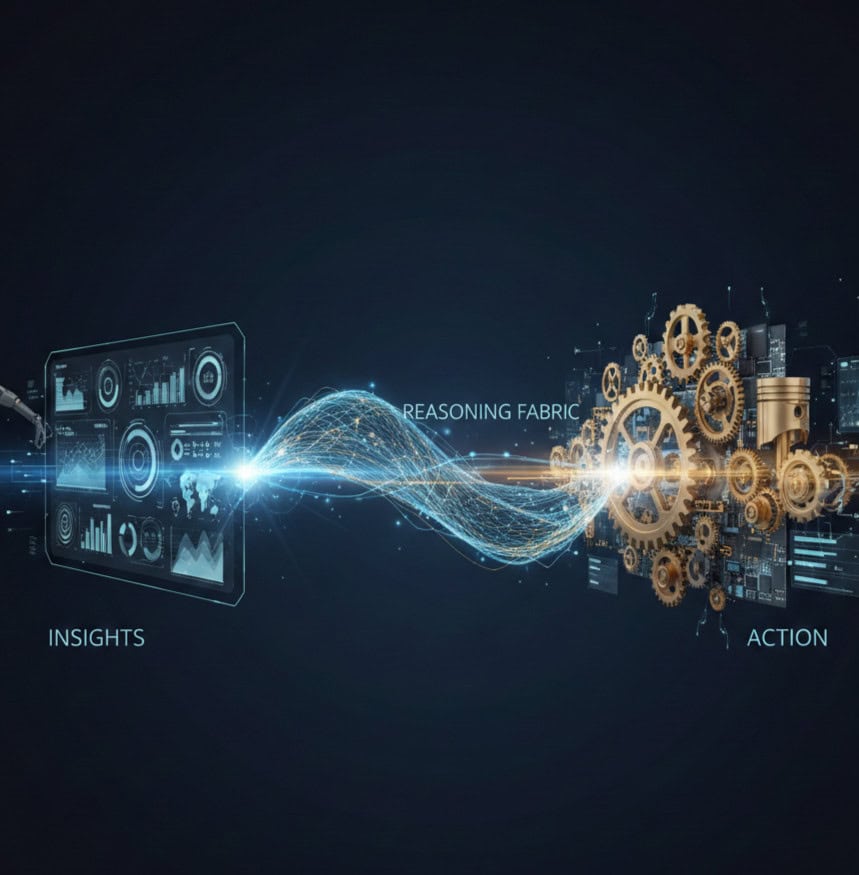

In most organizations, intelligence still stalls at the dashboard. Predictions fail to alter day-to-day operations, and